Taxes on Gifts and Inheritances

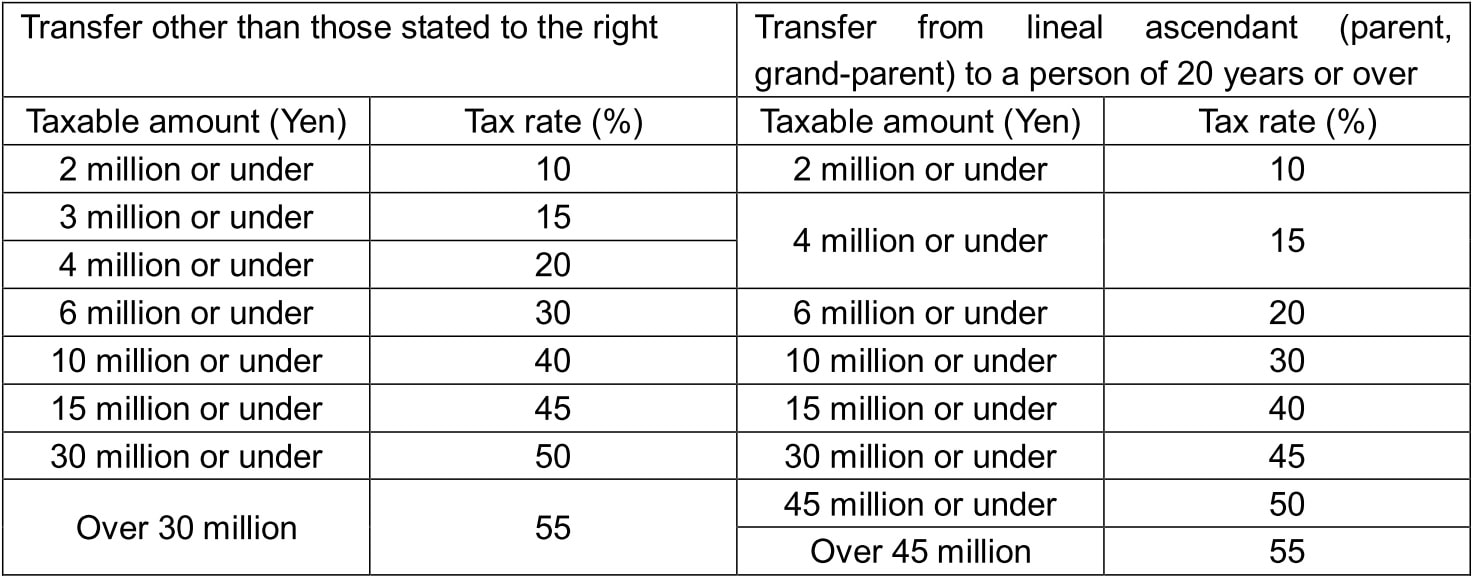

( 1 ) Gift Tax

Those who acquired property as a gift must file a return to pay gift tax in the period from February 1 to March 15 of the year following the acquisition of the property. The taxable value is the amount after deducting the basic allowance (¥1,100,000) and the special spouse allowance (¥20,000,000).

The donee who receives a gift from the parents or grandparents has an option to apply the inheritance tax adjustment system in which the donee pays smaller amount of tax on gifts and settles the final amount as inheritance tax later.

Those who acquired property as a gift must file a return to pay gift tax in the period from February 1 to March 15 of the year following the acquisition of the property. The taxable value is the amount after deducting the basic allowance (¥1,100,000) and the special spouse allowance (¥20,000,000).

The donee who receives a gift from the parents or grandparents has an option to apply the inheritance tax adjustment system in which the donee pays smaller amount of tax on gifts and settles the final amount as inheritance tax later.

Taxable amount and tax rate

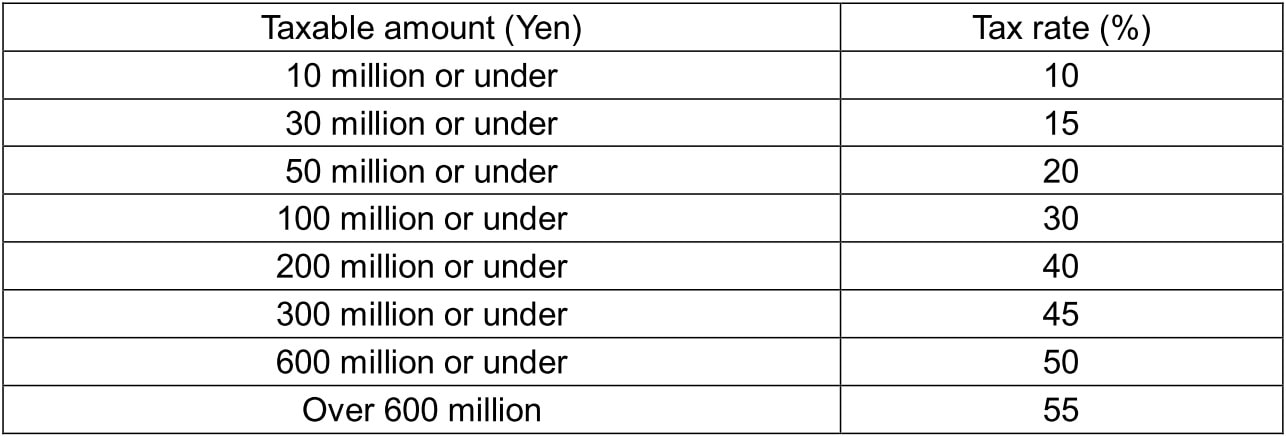

( 2 ) Inheritance Tax

Those who acquired properties by inheritance or bequest, and the total value of the properties exceeds the basic deductible allowance, must file a return to pay inheritance tax within, in principle, ten months after the date of the acquisition. The person who died is called the ancestor, and the person who inherited property is called the inheritor. The scope of property subject to inheritance tax varies depending on whether the inheritor’s address (domicile) is within or outside of Japan.

Those who acquired properties by inheritance or bequest, and the total value of the properties exceeds the basic deductible allowance, must file a return to pay inheritance tax within, in principle, ten months after the date of the acquisition. The person who died is called the ancestor, and the person who inherited property is called the inheritor. The scope of property subject to inheritance tax varies depending on whether the inheritor’s address (domicile) is within or outside of Japan.

Taxable amount and tax rate

* The amount of basic deductible allowance is 30 million yen plus 6 million yen times the number of legal heirs.