Capital Gain Tax

A capital gain is the profit realised on the sale of a property. Capital gains tax is charged on the taxable portion of the gain. Any gain is declared on your income tax statement as ‘other income‘ and is taxed separately to your own income. Both residents and non-residents (eg. those living overseas) are liable to pay this tax, although non-residents are not required to pay the municipal tax. Also, both foreign and domestic investors may be liable to pay consumption tax to the Japanese tax office upon the sale of Japanese property. This may include private individuals who were renting out their property to a tenant.

TAX RATE ; For Non-Residents (those living overseas):

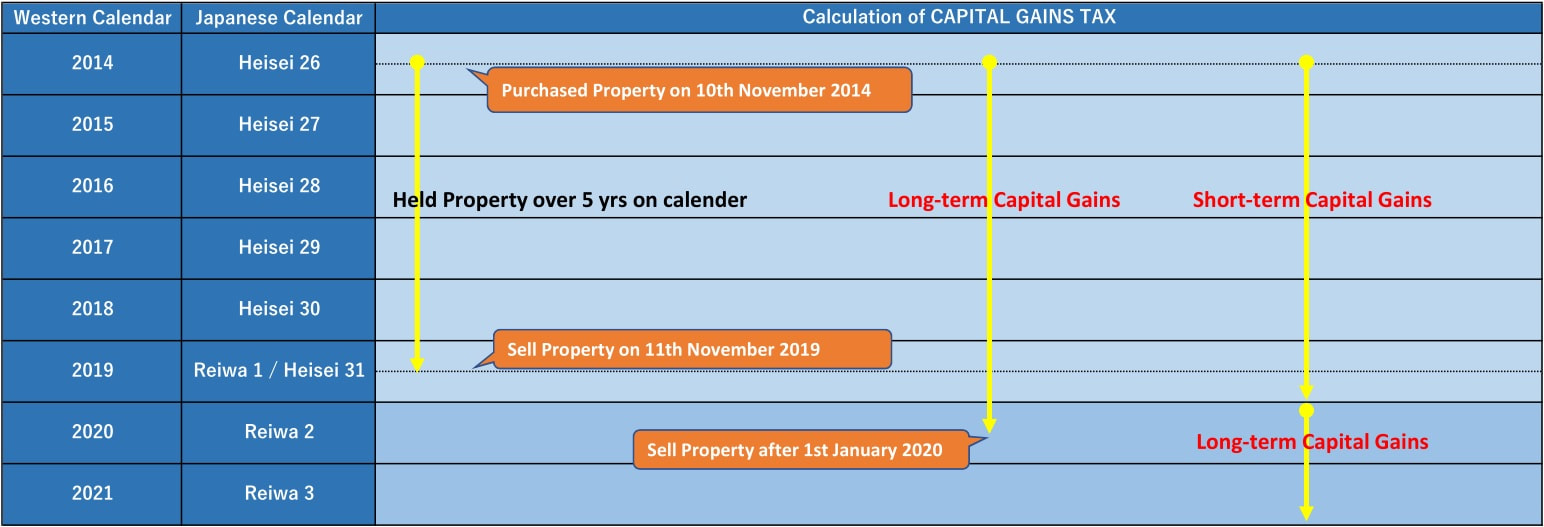

If held less than 5 years: 30% income tax + 2.1% Tohoku reconstruction tax (+ 9% municipal tax*¹ )

If held for more than 5 years: 15% income tax + 2.1% Tohoku reconstruction tax *²

If held for more than 5 years: 15% income tax + 2.1% Tohoku reconstruction tax *²

*1 If you are not a resident of Japan, in principle you are not required to pay municipal tax (juminzei). If you recently left Japan but held residence on January 1, then you may still be liable. Please check with a tax advisor.

*2 The special Tohoku reconstruction tax was introduced in 2013 and will be in effect until 2037. It applies to both residents and non-residents and is taxed based on the income tax amount of the sale rather than the total taxable capital gain value. See the examples below.

*2 The special Tohoku reconstruction tax was introduced in 2013 and will be in effect until 2037. It applies to both residents and non-residents and is taxed based on the income tax amount of the sale rather than the total taxable capital gain value. See the examples below.